Navigating the American health care system often feels like trying to solve a puzzle where the pieces keep changing shape. For many, health insurance is one of the largest monthly expenses in their household budget, yet it remains one of the least understood financial products. Whether you are self-employed, working a gig economy job, or simply looking for alternatives to an employer-sponsored plan, understanding the landscape of private health care is essential for your physical and financial well-being.

The stakes are high. Choosing the wrong plan can leave you underinsured in a medical emergency or overpaying for coverage you don’t need. With premiums rising and networks narrowing, the days of simply picking the “standard” option are over. Consumers must now act as their own advocates, analyzing deductibles, networks, and drug formularies to find a policy that fits their unique life stage.

This guide aims to demystify private health care in the United States. We will break down the alphabet soup of plan acronyms, explore what drives monthly costs, and provide actionable advice on selecting coverage that balances affordability with adequate protection. By the end, you will have the knowledge needed to make an informed decision during your next enrollment period.

Overview of Private Health Care Plans

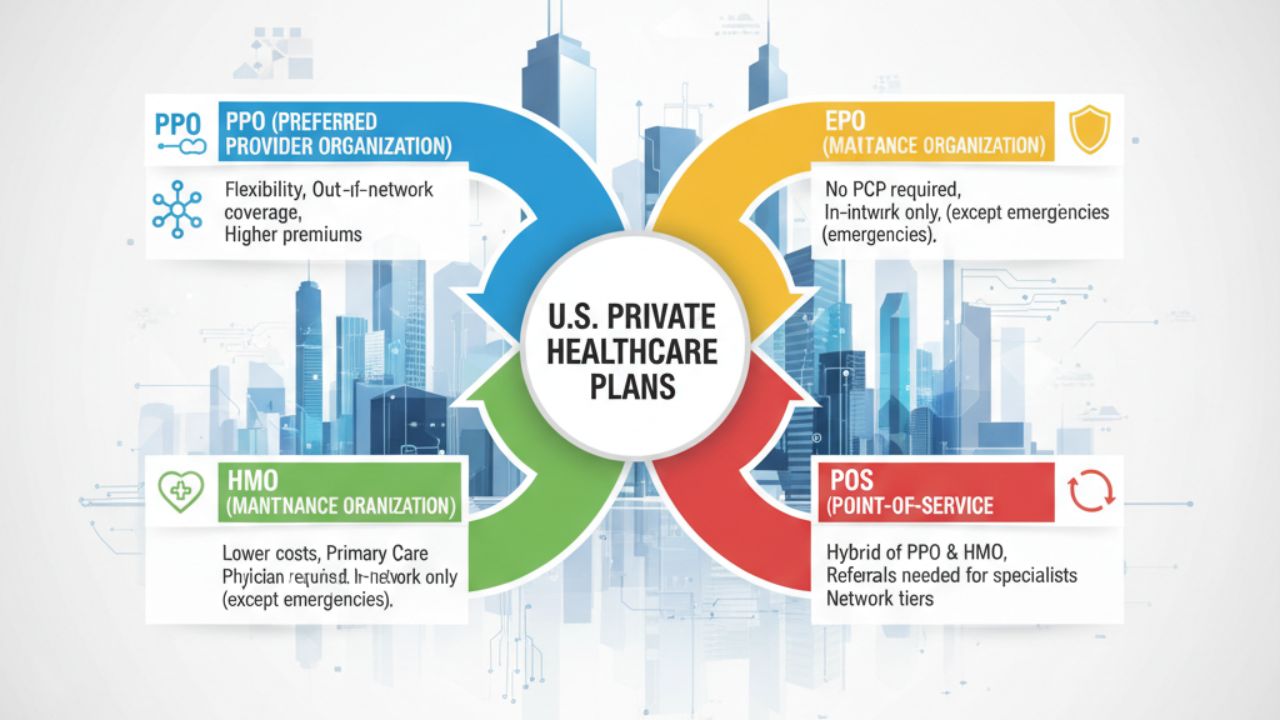

When shopping for private health insurance, usually through the Health Insurance Marketplace (Healthcare.gov) or directly through a provider, you will encounter four main types of plan structures. These structures dictate which doctors you can see and how much the insurance company pays.

Health Maintenance Organization (HMO)

HMOs are designed to keep costs low by limiting coverage to care from doctors who work for or contract with the HMO. generally, you must choose a Primary Care Physician (PCP). If you need to see a specialist, like a dermatologist or a cardiologist, you must get a referral from your PCP first.

- Pros: Usually have lower monthly premiums and lower out-of-pocket costs.

- Cons: Very restrictive. Except in a true emergency, out-of-network care is rarely covered. You have less freedom to choose your providers.

Preferred Provider Organization (PPO)

PPO plans offer the most flexibility. You have a network of “preferred” providers who have agreed to lower rates, but you can also see out-of-network doctors for an additional cost. You do not need a Primary Care Physician, and you do not need referrals to see specialists.

- Pros: Maximum freedom and flexibility. Great for people who travel or have specific specialists they want to see.

- Cons: These plans generally come with the highest monthly premiums and higher out-of-pocket costs if you go out-of-network.

Exclusive Provider Organization (EPO)

Think of an EPO as a hybrid that leans closer to an HMO. Like an HMO, you generally must stay within the network to get coverage (except for emergencies). However, like a PPO, you typically do not need a referral to see a specialist.

- Pros: Lower premiums than a PPO. No hassle with referrals.

- Cons: strict network boundaries. If you see a non-network provider, you are responsible for the full bill.

Point of Service (POS)

POS plans combine features of HMOs and PPOs. Like an HMO, you usually need to designate a Primary Care Physician and get referrals for specialists. However, like a PPO, you may have coverage for out-of-network care, though your share of the cost will be significantly higher.

- Pros: A middle-ground option that offers some out-of-network flexibility.

- Cons: The referral requirement can be a hurdle, and paperwork for out-of-network claims can be cumbersome.

Factors Affecting Monthly Costs

The sticker price of your health insurance—the premium—isn’t random. Under the Affordable Care Act (ACA), insurers can only use five specific factors to set premium rates for individual and small-group plans. Understanding these can help you anticipate your expenses.

Age

This is the most significant factor. Health care needs generally increase as we get older. Insurers can charge older people up to three times more than younger people. This “age rating” means a 60-year-old will see a vastly different price tag than a 25-year-old for the exact same policy.

Location (Rating Area)

Health care costs vary by zip code. This is due to the cost of living in that area, local legislation, and the level of competition among hospitals and doctors. A plan in rural Wyoming might cost significantly more than a comparable plan in urban Minneapolis due to a lack of provider competition.

Tobacco Use

Insurers can charge tobacco users up to 50% more than those who don’t use tobacco. This surcharge is one of the few behavioral factors insurers are allowed to consider. However, some states prohibit this or limit the percentage.

Individual vs. Family Enrollment

Naturally, a plan that covers just one person costs less than a plan covering a spouse and dependents. However, the cost isn’t always a simple multiplication; family deductibles and out-of-pocket maximums work differently than individual ones.

Plan Category (The Metal Tiers)

Plans are categorized by “metal” levels: Bronze, Silver, Gold, and Platinum. This doesn’t measure the quality of care, but rather how you and the insurer split the costs.

- Bronze: Lower monthly premiums, but you pay more when you get care (high deductible).

- Platinum: Highest monthly premiums, but the insurer pays more when you get care (low deductible).

Detailed Analysis of Coverage Options

While monthly premiums get all the attention, the true value of a plan lies in its coverage structure. Most comprehensive private plans must cover “Essential Health Benefits,” which include hospitalization, maternity and newborn care, mental health services, and prescription drugs. However, how you pay for these services varies.

Deductibles

This is the amount you pay for covered health care services before your insurance plan starts to pay. If your deductible is $2,000, you pay the first $2,000 of covered services yourself. After you pay your deductible, you usually pay only a copayment or coinsurance.

Copayments vs. Coinsurance

These are the payments you make after you’ve hit your deductible.

- Copay: A fixed amount ($20, for example) you pay for a covered health care service.

- Coinsurance: Your share of the costs of a covered health care service, calculated as a percent (for example, 20%). If a doctor’s visit is $100 and your coinsurance is 20%, you pay $20, and the plan pays $80.

Out-of-Pocket Maximum

This is the most critical safety net in your plan. It is the most you have to pay for covered services in a plan year. After you spend this amount on deductibles, copayments, and coinsurance, your health plan pays 100% of the costs of covered benefits. This protects you from financial ruin in the event of a catastrophic illness or accident.

Cost Comparison of Different Plans

To illustrate how these costs interact, let’s look at how the metal tiers typically break down. These figures are generalizations, as specific dollar amounts fluctuate wildly based on the factors mentioned earlier.

Bronze Plans:

- Premium: Lowest.

- Cost Sharing: You pay about 40%; the insurer pays 60%.

- Best For: Individuals who rarely see a doctor and want protection only against worst-case scenarios.

Silver Plans:

- Premium: Moderate.

- Cost Sharing: You pay about 30%; the insurer pays 70%.

- Best For: Moderate users. Importantly, Silver plans are the only ones eligible for “Cost-Sharing Reductions” (subsidies that lower your deductible/copays) if your income qualifies.

Gold Plans:

- Premium: High.

- Cost Sharing: You pay about 20%; the insurer pays 80%.

- Best For: People with regular medical appointments, chronic conditions, or expensive prescriptions.

Platinum Plans:

- Premium: Highest.

- Cost Sharing: You pay about 10%; the insurer pays 90%.

- Best For: Those who utilize health services very frequently and want the lowest possible costs at the point of care.

Tax Advantages and Savings

Private health care is expensive, but the tax code offers mechanisms to soften the blow. Utilizing these accounts can effectively reduce your medical expenses by 20% to 30%, depending on your tax bracket.

Health Savings Accounts (HSA)

An HSA is available only if you have a High Deductible Health Plan (HDHP). It offers a “triple tax threat”:

- Contributions are tax-deductible (lowering your taxable income).

- The money grows tax-free (if invested).

- Withdrawals are tax-free if used for qualified medical expenses.

Unlike other accounts, HSA funds roll over year to year. It is one of the most powerful retirement vehicles available, effectively acting as a dedicated 401(k) for healthcare.

Flexible Spending Accounts (FSA)

FSAs are generally offered through an employer, but relevant to understand in the broader context. You contribute pre-tax dollars to pay for copays, prescriptions, and other medical costs. The catch is the “use it or lose it” rule—funds generally must be spent by the end of the plan year.

Premium Tax Credits

If you buy insurance through the Marketplace, you may qualify for a tax credit that lowers your monthly premium. These subsidies are based on your estimated household income for the year. The American Rescue Plan and subsequent legislation have expanded these credits, making them available to more middle-income families than before.

Choosing the Right Plan for Your Needs

Selecting a plan is about risk management. You are essentially placing a bet on how much medical care you will need in the coming year. Here are a few scenarios to guide your choice:

Scenario A: The Young and Healthy

If you visit the doctor once a year for a physical and have no ongoing prescriptions, a Bronze plan or a high-deductible Silver plan is likely your best bet. Pairing this with an HSA allows you to save the money you would have spent on higher premiums.

Scenario B: The Growing Family

Kids are unpredictable. Between ear infections, sports injuries, and regular checkups, utilizing a PPO or a Gold plan can make sense. The higher premium buys you lower copays and the flexibility to see pediatric specialists without navigating a referral maze.

Scenario C: Managing Chronic Conditions

If you have diabetes, heart disease, or another condition requiring regular management, chasing the lowest premium is often a mistake. A low-premium Bronze plan with a $7,000 deductible means you will likely pay that full $7,000 out of pocket before coverage kicks in. A Gold or Platinum plan, despite the higher monthly cost, will cap your annual expenses sooner.

Tips for Lowering Health Care Costs

Regardless of the plan you choose, proactive management can keep costs down.

- Stay In-Network: This is the golden rule. Stepping out of your network is the fastest way to rack up massive bills. Always verify that a lab or anesthesiologist is in-network before a procedure.

- Shop for Prescriptions: Insurance copays aren’t always the cheapest price. Apps like GoodRx can sometimes offer lower prices on generic drugs than your insurance copay.

- Utilize Preventive Care: Under ACA rules, specific preventive services (like vaccines, mammograms, and cholesterol screenings) are free when provided by in-network doctors. Use them to catch problems early.

- Consider Telehealth: Many insurers offer lower copays for virtual visits compared to in-person urgent care trips. It’s an efficient way to handle minor ailments like rashes or sinus infections.

Future Trends in Private Health Care

The landscape of private health insurance is shifting beneath our feet, driven by technology and changing consumer demands.

Value-Based Care

The industry is slowly moving away from “fee-for-service” (paying for every test and visit) to “value-based care.” In this model, providers are paid based on patient health outcomes. This aims to reduce unnecessary procedures and focus on keeping patients healthy rather than just treating them when they are sick.

AI and Personalized Medicine

Insurers are beginning to use artificial intelligence to predict health risks and intervene earlier. While this raises privacy concerns, it also promises more personalized care plans that could lower costs by preventing chronic diseases from escalating.

Telemedicine Expansion

The pandemic proved that remote care works. Expect future insurance plans to integrate “virtual-first” options where your primary point of contact is digital, offering lower premiums for those willing to forgo the traditional waiting room experience.

Navigating Your Health Care Journey

Private health care in America is not a simple system, nor is it a static one. It requires active participation. The “best” plan is a moving target that changes as your health, income, and family structure evolve.

Take the time to compare not just the premiums, but the total cost of care. Look at the worst-case scenario (the out-of-pocket maximum) and ensure you have the savings to cover it. While the monthly cost is painful, health insurance remains the only firewall between a medical crisis and financial catastrophe. By understanding the mechanics of PPOs, deductibles, and tax credits, you empower yourself to make a choice that protects both your health and your future.